(Legal Framework Based on Jamabandi, Dhal Bach Maliya Mustaqil & Revenue Practice in Pakistan)

Introduction

Land cultivation revenue collection is the practical foundation for implementing AIT Tax (Advance Income Tax) on agricultural income in Pakistan. The AIT system does not operate independently; instead, it relies on verified land ownership, cultivation records, and assessed revenue data maintained through traditional land-revenue instruments such as Register of Rights (Jamabandi / رجسٹرِ حقوق) and Dhal Bach Maliya Mustaqil (ڈھال بچ مالیہ مستقل).

This article explains how Patwari, Qanungo, and Wasil Baki mechanisms collectively enable lawful, transparent, and enforceable AIT Tax implementation while protecting farmers and landowners from unjust taxation.

AIT Tax and Agricultural Land: Legal Context

AIT (Advance Income Tax) on agriculture is assessed using objective land-based indicators, not assumptions. These include:

- Cultivated land area (کاشت شدہ رقبہ)

- Ownership and possession status

- Nature of cultivation

- Assessed land revenue

Because agricultural income is land-linked, revenue records,not income declarations alone,form the legal base for AIT assessment. This approach differs fundamentally from urban income tax systems where self-declared income forms the primary basis. In agricultural contexts, the physical reality of land cultivation, verified through periodic inspections and recorded in official registers, provides objective evidence that prevents both tax evasion and unjust over-assessment.

The integration of traditional land revenue administration with modern tax requirements creates a unique system where centuries-old recordkeeping practices serve contemporary fiscal objectives. This continuity ensures that taxation respects actual agricultural capacity rather than arbitrary estimates.

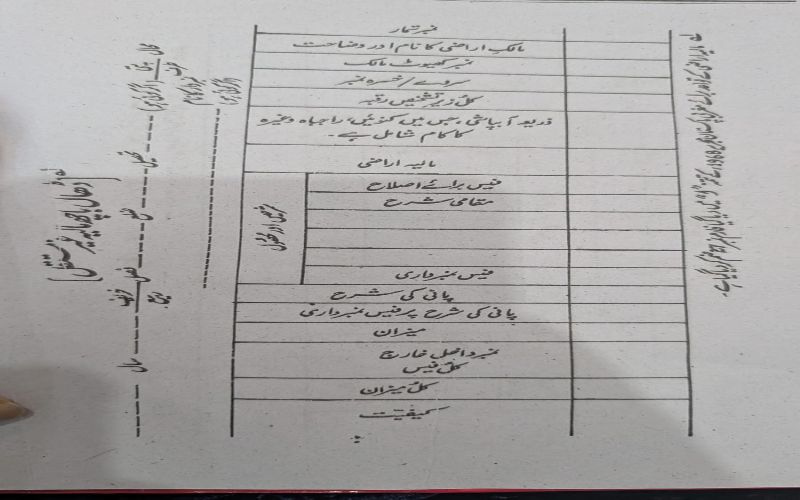

Register of Rights (Jamabandi / رجسٹرِ حقوق)

Central Role in AIT Implementation

The Register of Rights (Jamabandi) is the primary statutory land record, recording:

- Landowners (مالکان)

- Cultivators / tenants (کاشتکار / مزارع)

- Nature of rights and possession

- Assessed land revenue

For AIT purposes, Jamabandi establishes legal liability by identifying who owns and who cultivates the land. This distinction is crucial because agricultural income tax liability may differ between absentee landowners and actual cultivators depending on tenancy arrangements. In cases where land is cultivated under sharecropping or lease agreements, Jamabandi entries determine which party bears primary tax responsibility.

If Jamabandi is outdated or incorrect, AIT assessment becomes legally defective. This creates significant legal vulnerability for revenue authorities attempting to collect tax based on flawed records. Courts consistently require proof that tax assessments are grounded in accurate, up-to-date Jamabandi entries, making regular mutation updates essential not just for ownership clarity but also for lawful taxation.

Dhal Bach Maliya Mustaqil (ڈھال بچ مالیہ مستقل)

Permanent Revenue Assessment Instrument

Dhal Bach Maliya Mustaqil is a permanent land-revenue assessment form, prepared village-wise (موضع وار) by the Patwari, showing:

- Revenue demand against each landholder

- Distribution of liability

- Total payable amounts

This document is directly relevant to AIT Tax, because it reflects verified agricultural capacity, not estimated income. The Dhal Bach serves as an intermediary document that translates physical land characteristics,soil quality, irrigation access, crop patterns,into monetary revenue obligations. By establishing a baseline revenue demand, it creates a fair and transparent foundation for calculating additional agricultural income tax.

The preparation of Dhal Bach requires careful field verification because it affects not only current tax liability but also long-term assessment patterns. Once established, these assessments typically remain stable unless significant changes in land use or cultivation methods occur. This stability provides predictability for farmers while ensuring consistent revenue collection for the government.

Errors in Dhal Bach lead to:

- Over-taxation of farmers

- Under-collection of state revenue

- Administrative and disciplinary consequences

In practice, errors often arise from outdated cultivation data, failure to account for land lying fallow, or incorrect calculation of fractional shares in joint holdings. Such errors can cascade through the entire revenue system, affecting property tax assessments and creating legal disputes that take years to resolve.

Role of the Patwari (پٹواری)

The Patwari is the field-level foundation of land cultivation revenue collection. His responsibilities include:

- Maintaining Jamabandi

- Preparing Dhal Bach Maliya Mustaqil

- Recording cultivation data through Khasra Girdawari

- Issuing Parcha (پرچہ) to landowners and cultivators

- Assisting recovery of land revenue relevant to AIT

Patwari’s role extends beyond mere recordkeeping; he acts as the primary interface between agricultural landholders and the taxation system. During harvest seasons, Patwaris conduct field inspections to verify actual crop cultivation, assess yields, and update cultivation records. These ground-level observations form the factual basis for all subsequent revenue and tax calculations.

Under the transcribed rules, negligence or incorrect preparation of Dhal Bach or Parcha attracts strict disciplinary action. This accountability mechanism is essential because the Patwari’s entries directly determine tax liability for hundreds or thousands of farmers within his jurisdiction. Any manipulation, whether intentional or negligent, can result in significant financial harm to taxpayers or revenue loss to the state.

Supervisory Control by Qanungo (قانونگو)

The Qanungo provides verification and oversight, ensuring:

- Accuracy of Jamabandi entries

- Correct preparation of Dhal Bach

- Lawful recording of cultivation and revenue

For AIT implementation, the Qanungo acts as a quality-control authority, preventing manipulation at the Patwari level. This supervisory layer is particularly important given the Patwari’s direct contact with landholders, which creates opportunities for both genuine errors and potential corruption.

The Qanungo typically reviews Patwari records periodically, conducts spot checks of field data, and investigates complaints from taxpayers regarding incorrect assessments. When discrepancies are found, the Qanungo has authority to order corrections and, in serious cases, recommend disciplinary proceedings. This oversight ensures that AIT Tax remains grounded in verified facts rather than arbitrary or influenced data.

Wasil Baki (واسل باقی): Outstanding Revenue & AIT Linkage

Wasil Baki represents outstanding land revenue or dues that remain unpaid.

In AIT-linked systems, Wasil Baki helps authorities:

- Identify unpaid agricultural liabilities

- Track recoverable revenue

- Prevent concealment of taxable agricultural capacity

Proper Wasil Baki maintenance ensures complete and fair AIT enforcement. When landholders accumulate unpaid revenue over multiple years, it signals either financial distress or deliberate tax avoidance. Revenue authorities use Wasil Baki records to prioritize recovery efforts, negotiate payment plans, or initiate legal proceedings when necessary.

The connection between historical revenue arrears and current AIT liability is important because consistent non-payment may indicate that land is not being productively cultivated, which affects future tax assessments. Conversely, cleared Wasil Baki demonstrates financial capacity and strengthens the case for applying standard AIT rates without seeking exemptions or reductions.

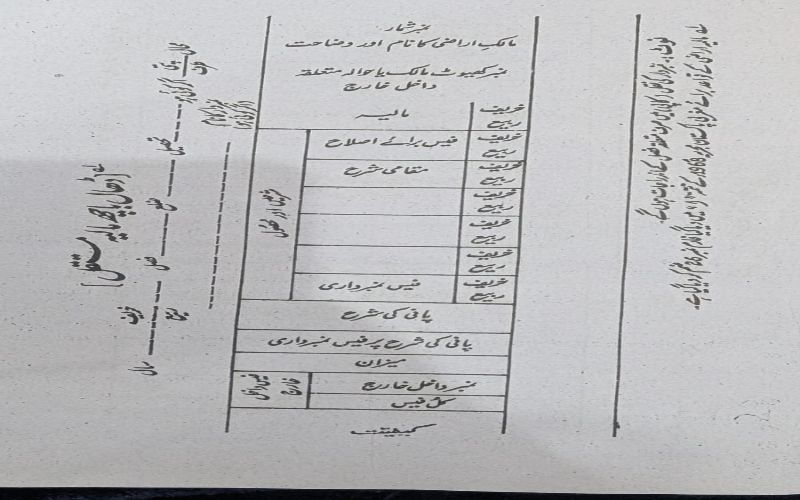

Parcha (پرچہ): Transparency Tool for AIT

Purpose of Parcha

A Parcha is an official land-revenue slip issued by the Patwari containing:

- Complete cultivation and revenue entries

- Details drawn from Jamabandi and Dhal Bach

- A signed record acknowledged by the landholder

Parche provide transparency, enabling taxpayers to verify the data used for AIT assessment. In an environment where many farmers have limited literacy and minimal access to formal legal resources, the Parcha serves as their primary documentary proof of what authorities claim they owe. This simple receipt-like document empowers landholders to challenge incorrect assessments before they escalate into enforcement actions.

Authority and Distribution of Parche

- Normally issued on demand

- After settlement, distributed to all landowners and cultivators

- In special cases, distribution may be ordered by the Collector (کلکٹر) through Revenue Courts or Revenue Authorities

This ensures uniform access to AIT-relevant information. The requirement for distribution after settlement prevents situations where authorities complete tax assessments without informing affected parties, which would violate basic principles of administrative fairness and due process.

Free Annual Entries and Taxpayer Protection

Under the revenue rules:

- Every landowner or cultivator has the right to obtain annual entries free of charge

- These entries may be demanded before Parcha issuance or tax assessment

- No fee can be charged by the Patwari

This provision prevents hidden manipulation of AIT-linked records. By guaranteeing free access to one’s own land record entries, the system reduces information asymmetry between taxpayers and authorities. Farmers can verify that cultivation data, ownership status, and revenue assessments recorded in official registers match ground reality before these records are used for tax calculation.

The prohibition on charging fees is particularly significant because it removes a common source of petty corruption and ensures that even the poorest landholders can access information necessary to protect their rights. This accessibility strengthens the legitimacy of the entire AIT system by demonstrating that it operates transparently and fairly.

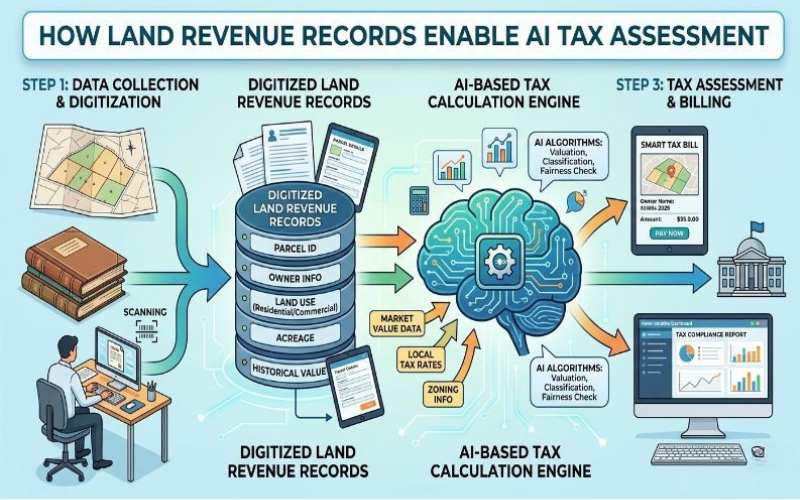

How Land Revenue Records Enable AIT Tax

The AIT framework functions through an integrated revenue chain:

- Jamabandi → defines ownership & cultivation

- Patwari → prepares cultivation & revenue data

- Qanungo → verifies accuracy

- Wasil Baki → tracks unpaid dues

- Collector / Revenue Courts → enforce recovery

This structure ensures AIT Tax is lawful, evidence-based, and defensible. Each component serves as a check on the others, creating a system of mutual accountability. When properly implemented, this chain prevents both arbitrary taxation and large-scale evasion, achieving a balance between revenue collection objectives and taxpayer protection.

The strength of this system lies in its integration of administrative, legal, and fiscal functions. Unlike modern tax systems where different agencies handle assessment, collection, and enforcement separately, Pakistan’s agricultural tax framework consolidates these functions within the land revenue administration, enabling faster dispute resolution and more efficient compliance monitoring.

Why This System Matters

Accurate land cultivation revenue collection:

- Protects farmers from unjust taxation

- Reduces agricultural tax evasion

- Strengthens government revenue

- Builds trust in land and tax administration

Beyond these immediate benefits, the system preserves valuable institutional knowledge accumulated over generations of land administration. The detailed cultivation records, soil assessments, and irrigation data maintained through this framework serve purposes far beyond taxation, supporting agricultural planning, land disputes resolution, and rural development initiatives.

When farmers trust that their tax liability is calculated fairly based on verifiable records rather than arbitrary assessments, they are more likely to comply voluntarily and less likely to invest resources in evasion strategies. This trust is the foundation of effective agricultural taxation and sustainable rural development.

Conclusion

Land cultivation revenue collection through Register of Rights (Jamabandi), Dhal Bach Maliya Mustaqil, Parcha issuance, and Wasil Baki recovery forms the legal backbone for implementing AIT Tax on agricultural income in Pakistan. The coordinated roles of Patwari, Qanungo, and Collector ensure that agricultural taxation remains fair, transparent, and legally sound.

This centuries-old system, when properly maintained and honestly administered, provides a model for how traditional governance structures can effectively support modern fiscal requirements while protecting the rights and livelihoods of agricultural communities.