Most landowners in Pakistan know they are supposed to pay land revenue, but very few understand how that amount is actually calculated, recorded, and linked to their specific holding. Village Form II is the document at the center of that process, and understanding it properly can save you from overpaying, underpaying, or running into complications during a property transaction or dispute.

The Assessment Register Every Landowner Should Know About

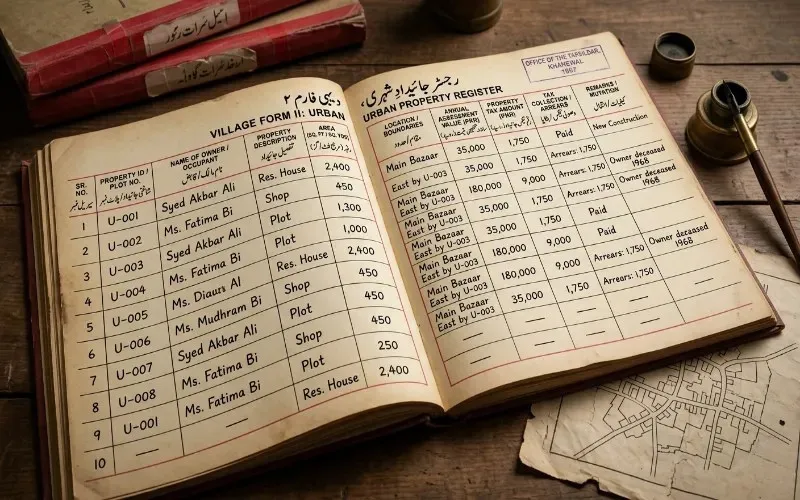

Village Form II is the land assessment and revenue demand register maintained by the Patwari for each revenue estate. It records the officially assessed value of every landholding within a Deh and the corresponding land revenue demand levied against it. In plain terms, it is the document that tells the government how much revenue each piece of land owes, and it tells the landowner what they are legally liable to pay.

The form is part of the same family of village registers that includes Form VII for ownership and the Khasra Girdawari for cultivation data. Each form captures a different layer of the land record, and Form II specifically focuses on fiscal liability rather than ownership or possession.

What Village Form II Actually Contains

Before looking at how the form is used in practice, it helps to understand exactly what information it records. The entries in Form II are organized around each survey number within the revenue estate, and the data is updated at each revenue settlement cycle.

The key fields recorded in Village Form II include the following:

- The survey number and Hissa number of the landholding

- The area of the holding in kanals, marlas, or acres depending on the province

- The classification of the land, whether irrigated, rain-fed, or cultivable waste

- The assessed annual land revenue demand for that holding

- The name of the person liable to pay the revenue, which corresponds to the owner recorded in Form 7-A

- Any remissions or concessions applied to the demand, such as exemptions for small holdings

- The cumulative record of payments made and any outstanding arrears

The connection between Form II and ownership is direct. The person recorded as liable to pay in Form II is drawn from the ownership entries in Village Form VII. When ownership changes through a mutation, the revenue liability in Form II is updated to reflect the new owner’s name.

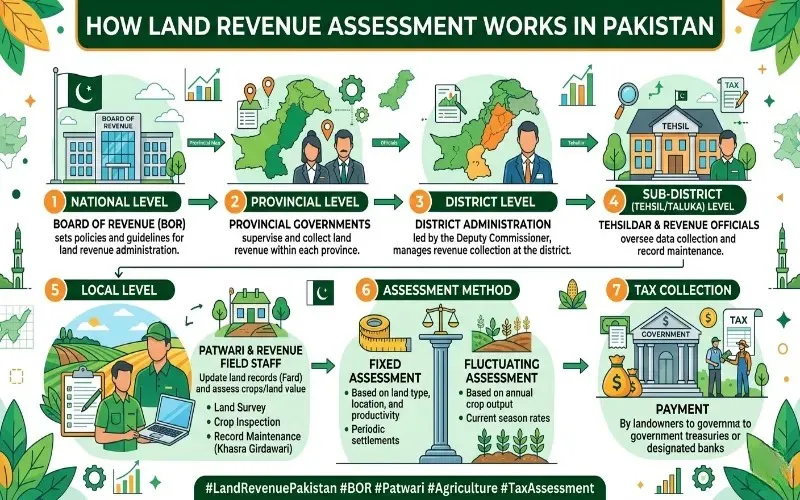

How Land Revenue Assessment Works in Pakistan

Land revenue in Pakistan is not calculated property by property on market value the way urban property tax is. It is assessed through a periodic settlement process conducted by the provincial revenue department. Understanding this process explains why Form II looks the way it does and why the amounts recorded in it may seem disconnected from current land prices.

During a revenue settlement, government surveyors and settlement officers classify each survey number in a district based on soil quality, water availability, and productivity. Irrigated land in fertile zones is assessed at a higher rate than rain-fed or dry land. This classification is recorded against each survey number and becomes the basis for calculating the annual land revenue demand entered in Form II.

The land revenue collection guide covers how these demands are collected by revenue officials across Pakistan’s rural districts. Form II is the document that originates those demands at the village level before they are consolidated into district-level revenue rolls.

The Difference Between Land Revenue and Property Tax

Many people use land revenue and property tax interchangeably, but they are legally distinct in Pakistan’s fiscal system. Knowing the difference matters because they are administered by different authorities, follow different rules, and are recorded in different documents.

Land revenue is a provincial levy on agricultural land, assessed through the settlement system and recorded in Form II. It is administered by the Board of Revenue and collected through the Patwari and Tehsildar hierarchy. It applies to rural agricultural holdings and is calculated based on land classification, not market value.

Property tax, on the other hand, is levied on urban properties by municipal and local government authorities. It is based on the annual rental value or capital value of the property and is recorded in municipal tax registers rather than village revenue forms.

The practical consequence is that if you own agricultural land in a rural Deh, your fiscal liability is recorded in Form II as land revenue. If you own a house or commercial plot in a city, your liability falls under the urban property tax system in Pakistan, which follows an entirely separate process. Some landowners straddle both systems when they hold agricultural land that has been reclassified or sits near urban boundaries.

How Arrears in Form II Affect Property Transactions

One of the most practically important aspects of Form II is what happens when land revenue is not paid. Unpaid land revenue accumulates as arrears in the Form II register, and those arrears become a charge on the land itself, not just a personal debt of the owner.

This means that when land is sold, the arrears travel with the land unless they are settled before the transfer. A buyer who purchases land without checking the Form II arrears column inherits those unpaid dues. Revenue law in most provinces allows the government to recover land revenue arrears from whoever currently holds the land, regardless of when the debt was incurred.

Before completing any sale, the seller should obtain a clearance confirming no outstanding land revenue demand exists against the survey number. Verifying this through the Patwari or Tehsildar is a step that belongs alongside checking the ownership record and the mutation status. Fraud and manual errors in property records are not limited to ownership documents. Arrear records can also carry errors that unfairly burden a new buyer.

Land Classification and Its Impact on Assessment

The classification recorded against each survey number in Form II is one of the most consequential entries in the entire register. A change in classification, such as when land is brought under canal irrigation or when cultivable waste is developed into productive farmland, can significantly alter the revenue demand.

In Sindh, land is broadly classified into categories based on water source and crop potential. Perennial canal-irrigated land carries the highest assessment, followed by seasonal canal land, tube well-irrigated land, and rain-fed land. Cultivable waste and barren land attract nominal or zero revenue demand.

This classification system also intersects with the question of converting agricultural land into a residential plot. When agricultural land is formally reclassified for urban use, it moves out of the land revenue system and into the property tax system. Until that reclassification is formally processed, Form II continues to record it as agricultural land with its original revenue demand.

Remissions and Exemptions Recorded in Form II

Not every landowner pays the full assessed demand recorded in Form II. Provincial governments regularly grant remissions, which are partial or full reductions in the revenue demand, under specific circumstances. These remissions are recorded directly in Form II against the relevant survey numbers.

Common grounds for remission include the following situations:

- Crop failure due to flood, drought, or pest damage

- Land falling out of cultivation due to waterlogging or salinization

- Holdings below a minimum threshold size that qualify for exemption under provincial rules

- Land owned by widows or other categories granted relief under provincial policy

Understanding these remissions matters because they affect the actual amount owed. A Form II entry showing a high assessed demand but with a remission notation means the effective liability is lower. Verifying the net demand after remissions is important before settling arrears or completing a transaction.

The Patwari’s Role in Maintaining Form II

The Patwari maintains Form II as part of their core record-keeping duties within the Halqa. They update it when ownership changes through mutation, when land classification changes after a field inspection, and when payments are received and credited against the demand.

The duties of a Patwari in Pakistan include presenting Form II during revenue inspections by the Qanungo and the revenue officer, issuing payment receipts to landowners, and ensuring that arrear entries are accurately maintained. Errors in Form II entries, particularly incorrect arrear amounts or misattributed demands, are a known source of problems during property transactions and should be corrected through a formal application to the Tehsildar.

The Qanungo in revenue administration supervises Patwari records across multiple Halqas and conducts periodic inspections to ensure Form II entries are current and accurate. If you suspect your Form II record has an error, approaching the Qanungo is often faster than waiting for the Patwari to self-correct.

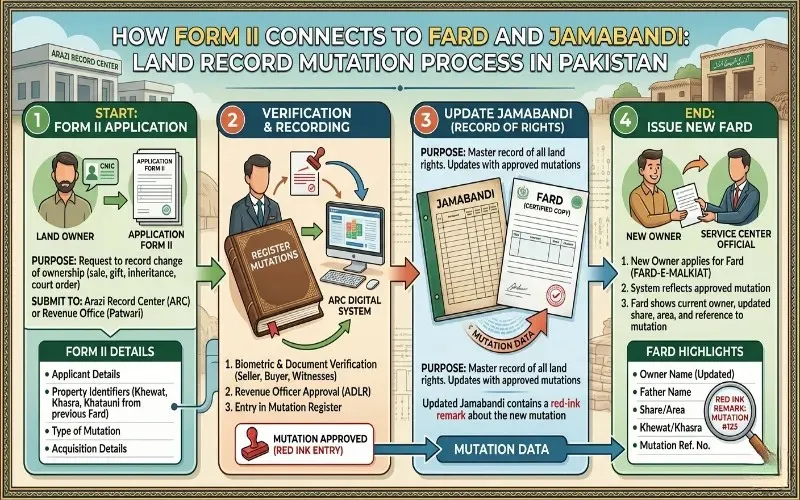

How Form II Connects to the Fard and Jamabandi

Village Form II does not exist in isolation. It draws from and feeds into other core land records in ways that make understanding those connections practically useful.

The ownership entries in Form II, specifically the name of the person liable for revenue, are drawn from Form 7-A of Village Form VII. When a mutation updates the ownership record, the revenue liability in Form II must also be updated to reflect the new owner. If a mutation has been sanctioned but Form II has not been updated, the revenue demand may still appear under the previous owner’s name, which can create confusion during transactions.

The Jamabandi in revenue consolidates ownership data from Form VII and the revenue demand from Form II into a single authenticated record of rights at each four-year revision cycle. A Fard issued to a landowner reflects the ownership side of this combined record, while the revenue demand side remains in Form II as the active fiscal register between Jamabandi revisions. The difference between Jamabandi and Intkal helps clarify how transfers recorded through mutation eventually become part of the authenticated ownership picture that Form II draws its liability names from.

Getting a Certified Copy and Settling Dues

If you need a certified copy of your Form II entry, the process follows the same route as other village form requests. Approach the Patwari of your Halqa with your CNIC, survey number, and Deh name. The Patwari will provide a certified extract showing the assessed demand, any remissions applied, and the arrear status.

To settle outstanding land revenue dues, payment is made at the Tehsildar office or through designated bank branches depending on the province. After payment, the receipt is presented to the Patwari for entry into Form II, clearing the arrear against your survey number. Always retain the original payment receipt because it serves as proof of clearance in any future transaction or dispute involving that holding.

If you are managing an inheritance situation and need to account for all land revenue liabilities of the deceased before dividing property among heirs, obtaining the Form II status for every survey number in the estate is an essential early step.

Frequently Asked Questions

What is Village Form II in Pakistan’s land revenue system

Village Form II is the land assessment and revenue demand register maintained by the Patwari for each revenue estate. It records the officially assessed annual land revenue demand against every survey number in the village, along with the name of the liable owner, the land classification, any remissions applied, and the status of payments and arrears. It is the document from which land revenue dues are calculated and tracked at the village level, and it connects directly to the ownership entries in Village Form VII.

How is the land revenue demand in Form II calculated

The demand in Form II is calculated through a periodic revenue settlement process conducted by the provincial revenue department. Settlement officers classify each survey number based on soil quality, water source, and agricultural productivity. Irrigated and high-yield land is assessed at higher rates, while rain-fed, dry, or waste land attracts lower or nominal demands. The assessed rate per unit area is then applied to the total area of each holding to produce the annual demand recorded in Form II. This assessment is revisited at each new settlement cycle, which may occur every several decades.

Do unpaid land revenue arrears in Form II transfer to a new buyer

Yes. Land revenue arrears in Pakistan are a charge on the land itself rather than a personal liability of the owner alone. When land is sold without settling outstanding arrears, the new owner inherits those dues and the revenue department can recover them from the current holder. This is one of the most important reasons to verify the Form II arrear status before completing any property purchase. A clearance certificate from the Tehsildar confirming no outstanding demand is the safest way to confirm the record is clean before a transfer.

What is the difference between land revenue recorded in Form II and urban property tax

Land revenue recorded in Form II is a provincial levy on agricultural land administered by the Board of Revenue. It is assessed through the settlement system based on land classification and productivity, and it applies to rural agricultural holdings. Urban property tax is a separate levy administered by municipal authorities and calculated on the annual rental or capital value of urban properties. The two operate under different laws, are collected by different departments, and are recorded in different registers. A landowner whose agricultural land falls near or within an urban boundary may have obligations under both systems depending on how the land is classified.

What happens to Form II when agricultural land is converted to residential use

When agricultural land is formally reclassified for residential or commercial use through the relevant provincial and municipal approval process, it moves out of the land revenue system and into the urban property tax system. The Form II entry for that survey number is closed or marked as reclassified, and the land’s fiscal obligations shift to the municipal authority. Until the formal reclassification is completed and processed through the revenue department, Form II continues to record the land as agricultural with its original assessed demand. Paying land revenue after reclassification is approved but before the record is updated is a common transitional issue that should be clarified with the Tehsildar.